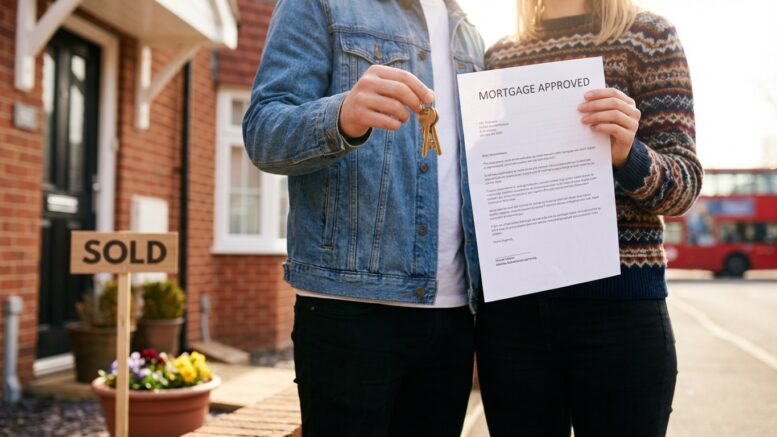

The number of 95 percent loan-to-value mortgages has reached its highest level since March 2008, giving more renters a path to homeownership and potentially affecting tenant demand in the private rented sector.

Data from Moneyfacts shows 537 mortgage products are now available at 95 percent LTV, nearly double the 274 products on offer in February 2024. Two-year fixed rates at this level start at around 4.47 percent, while five-year fixes begin at approximately 4.53 percent.

Lenders push beyond traditional thresholds

Several lenders have moved beyond the traditional 95 percent ceiling. Santander has launched a 98 percent LTV mortgage requiring a minimum £10,000 deposit, while Skipton Building Society offers a 100 percent product and Yorkshire Building Society has introduced a 99 percent option. These products typically carry specific eligibility criteria and property restrictions.

For landlords, the expansion represents a double-edged sword. While first-time buyer activity has already reached a 20-year high, suggesting some tenants are successfully transitioning to ownership, sustained rental demand from those who cannot yet save deposits remains strong.

Rachel Springall, finance expert at Moneyfacts, said: “This year is setting itself up to be a fruitful one for first-time buyers, and really, they need all the help they can get amid the lack of affordable housing.”

Half of aspiring buyers yet to seek advice

Research from the Building Societies Association reveals a significant awareness gap among potential buyers. Some 47 percent of aspiring homeowners have never consulted a lender or mortgage broker to assess their options, while 46 percent of those who had sought advice had not done so in the past year.

When informed about low-deposit and zero-deposit products available from building societies, two-thirds of respondents said they could purchase property sooner than they had previously anticipated. The BSA described this as “a clear gap between perception and reality” in the mortgage market.

The findings suggest many current renters may not realise they could afford to buy, which could affect landlord tenant retention rates as more discover the expanding range of purchase options available.

Deposit barriers remain for many

Despite the product expansion, deposit accumulation remains the primary obstacle for many renters. With rent and living costs consuming significant portions of monthly income, saving even a 5 percent deposit on the UK’s average £300,000 house price – requiring £15,000 – remains challenging for many households.

The BSA research indicates that targeted information about available products could accelerate the transition from renting to buying for some tenants. For landlords in areas with high first-time buyer activity, this may mean shorter tenancies and increased turnover, though the broader shortage of affordable housing continues to sustain rental demand nationally.

Editor’s view

More mortgage options for first-time buyers should, in theory, drain the tenant pool. In practice, house prices have grown faster than deposit savings for most renters, and the structural shortage of homes means demand remains strong across both tenures. Landlords should expect some churn as the most financially prepared tenants exit to buy – but not a cliff edge.

Author: Editorial Team – UK landlord & buy-to-let news, policy, and finance

Published: 13 February 2026

Sources: Moneyfacts, Building Societies Association

Related reading: First-time buyers hit 20-year high as renters become homeowners